The Impact of COVID-19 on Financial Reporting

April 27, 2020

Introduction

A novel strain of Coronavirus (COVID-19) which was first reported in late December 2019, quickly spread across all continents affecting most countries in the world by January 2020. It was declared as a global pandemic by the World Health Organisation (WHO) in March 2020. The rapid spread of the virus has vastly impacted the economy of almost all countries as a result of the lockdown imposed by many countries, reduction in consumption, cutbacks in production, restrictions in trade, travel bans and an overall contraction of economic activity.

In these unprecedented times, preparers of financial statements need to be aware of how these events affect the financial statements. This article summarises the main impacts of COVID-19 on the financial reporting and the main issues practitioners will need to consider in the Maldivian Context.

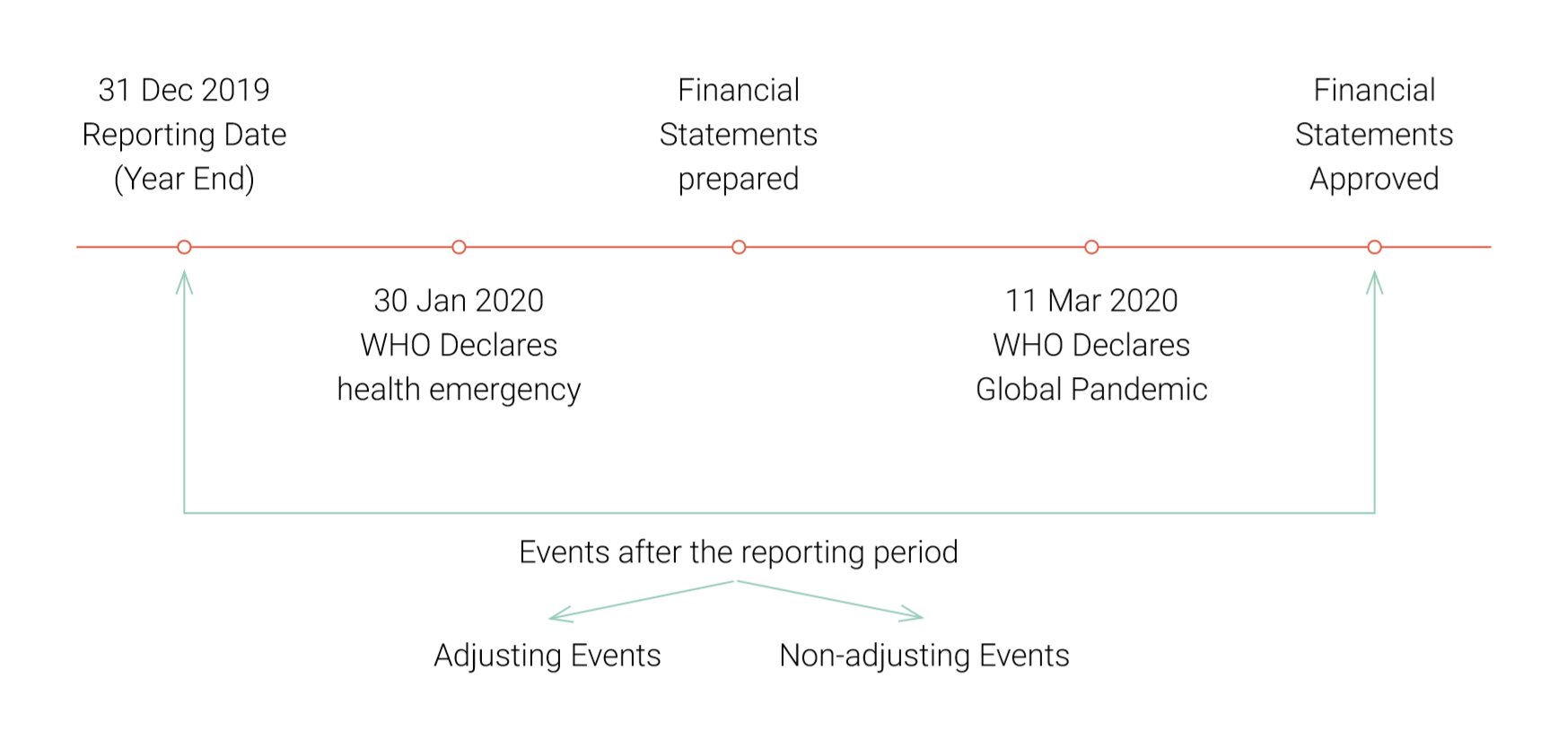

Adjusting or non-adjusting event

In preparing the financial statements entities are required to consider both favourable and unfavourable events that occur after the reporting date. In the context of IAS 10 Events after the reporting period, an adjusting event is an event that provides evidence of conditions that existed at the reporting date and a non-adjusting event indicates conditions that arose after the reporting date.

The COVID-19 was first reported to WHO as a novel virus on 31 December 2019 and it spread globally from January 2020 onwards, which resulted in countries taking strict measures to prevent the spread of the virus and contain the outbreak. The global spread of COVID-19 and the related control measures by the governments were taken after the end of 2019 and therefore, any impact due to COVID-19 for an entity with a reporting year ending 31 December 2019 would be a non-adjusting event.

In the case of a non-adjusting event, entities need to consider the impact of the non-adjusting event on the financial statements. If the impact is material, the entity should disclose the nature of the events and its estimated financial effect or a statement that such an estimate cannot be made.

For example, the bankruptcy of a customer that occurs after the reporting period due to the spread of the virus alone, will not require any adjustment in the financial statement. This is because there was no evidence of existing credit issues at the reporting date. Your professional judgement might be required in such situations.

Even though, COVID-19 would be a non-adjusting event for an entity with a reporting period ending 31 December 2019, entities with reporting period on or after 31 January 2020 should incorporate the effects of the COVID-19 in the preparation of financial statements. More importantly, entities should consider the adjustments relating to Impairment of Financial Instruments (IFRS 9), Impairment of assets (IAS 36) and Leases (IFRS 16).

Going concern

IAS 1 requires management to assess an entity’s ability to continue as a going concern when preparing the financial statements and the entity shall prepare financial statements on a going concern basis unless management either intends to liquidate the entity or to cease trading or has no realistic alternative but to do so.

In light of the impact of COVID-19 pandemic, management must carefully consider the assessment of the entity’s ability to continue as a going concern. In evaluating the entity’s ability to continue as a going concern, entities need to consider the current economic condition and the uncertainty of the situation. In addition to the general areas considered, the entity should also consider economic relief packages offered by the government including the entity’s eligibility to those reliefs and special schemes offered by financial institutions.

Where management is aware, in making its assessment of material uncertainties related to events or conditions that may cast significant doubt upon the entity’s ability to continue as a going concern, the entity shall disclose those uncertainties.

Where the management concludes that the entity will not survive 12 months from the reporting date, the entity shall not prepare the financial statements on a going concern basis. In this case, the entity shall disclose that fact, together with the basis on which it prepared the financial statements and the reason why the entity is not regarded as a going concern.

Impairment of Financial Instruments

With respect to IFRS 9 Financial Instruments, entities need to recognise the amount of Expected Credit Losses (ECL) on financial assets such as debt securities, lease, receivables and loans. ECL is a probability-weighted estimate of credit losses determined by evaluating a range of possible outcomes at the reporting date based on past events, current conditions and forecasts of future economic conditions (IFRS 9, paragraph 5.5.17).

Due to the COVID-19 pandemic, borrowers may be facing liquidity issues resulting in defaults or delays in repayment. These delays and defaults may imply a significant increase in the credit risk of the borrower and resulting in a change in the stage the financial assets are graded (stage one – 12 months ECL to stage two – lifetime ECL). Furthermore, the estimated fair value of the collateral may also show declines causing a higher ECL provision.

In the existing business environment of most entities’ selling goods and providing services may have huge trade receivables in their accounts. As trade receivable meets the definition of a financial instrument, it will be subject to IFRS 9. If these entities expect that their customer will pay later than agreed or not make any payments, then an impairment loss on trade receivable will need to be recognised. If an entity’s trade receivables do not contain a significant financing component, then that entity can recognize lifetime expected credit losses right on initial recognition.

Impairment of assets

As per IAS 36 Impairment of Assets, entities are required to assess whether there is any indication that an asset may be impaired (i.e. its carrying amount may be higher than its recoverable amount) at the end of each reporting period. The impact of COVID-19 has resulted in a decrease in economic activity and a fall in revenue for most entities which include indications of impairment. Therefore, entities need to perform impairment testing of their assets at the end of the reporting period (in addition to the requirement to perform an impairment test at least annually of goodwill and intangible assets with an indefinite useful life). It is important that entities incorporate the effects of COVID-19 in its assumptions, cash flows, and projections especially in the calculation of Value In Use.

Leases

In relation to COVID-19, landlords (lessors) have been offering rent concessions to tenants (lessees) in the form of rent holidays, deferment of rent payments and/or lower lease payments. In the current situation, it is also common that lessee may seek for early lease termination. Under IFRS 16 Leases, entities need to assess whether the change in payments is a lease modification or not. This distinction is important as the change in payments could be just a variable lease payment – recognising the effect of the concession as income or expense in the period in which they arise.

IFRS 16 defines a lease modification as a change in the scope or consideration for a lease, that was not part of the original terms and conditions of the lease. A change in the scope for a lease is considered where there is a change in the right of use conveyed to the lessee in the contract. For example, an extension of the contract term will be considered as a change in scope whilst a rent holiday is not a change in the scope of the contract. A change in the consideration for a lease is considered where there is a change in the overall effect of the lease payment. A rent deduction for 3 months in return for a higher amount in the later period of the lease will not be considered as a change in consideration.

If there is a change in the scope or consideration, the entity shall then consider if there is a rent concession in the original lease contract that can be applied to the current circumstances (e.g. by a force majeure clause) or applicable law or regulation. In such cases, there is no lease modification.

Apart from this, entities also need to consider the impact of COVID-19 on impairment of lessee’s right of use (ROU) assets or lessors held for lease assets, abandonment of ROU assets, lessee discount rates, lessee reassessments and fair value of underlying assets and ROU assets when accounting for leases.

In light of the many challenges practitioners are facing, the International Accounting Standards Board (IASB) has proposed an amendment to IFRS 16 Leases. The Exposure Draft Covid-19-Related Rent Concessions, published on 24th April 2020, proposes an amendment to permit lessees not to assess whether particular COVID-19-related rent concessions are lease modifications. Instead, lessees can account for those rent concessions as if they were not lease modifications. The Exposure Draft proposes no change for lessors and is open for public comment until 8 May 2020.

Other Matters

With lower demand, disrupted supply chains, restructuring plans, the introduction of government stimulus packages and possible bailouts, entities also need to consider the impact to financial statements due to other areas such as;

- Government Assistance (IAS 20)

- Onerous Contracts (IAS 37)

- Net realisable value of inventory (IAS 2)

You can download a PDF version of this issue from the link below: